Falling Yields Should Help Stocks… Right?

While the S&P 500 continues to hover near the psychologically important 7,000 level, another major market variable has been quietly moving in the opposite direction. The 10-Year Treasury Yield has been slipping away from its own defining level of the past few years — roughly 4.2%.

If we simply apply the playbook that has worked since the 2022 market bottom, this development should be supportive for equities. Over the last several years, falling yields and a softer U.S. dollar have consistently acted as tailwinds for risk assets. In fact, many of the market’s strongest advances since late 2022 occurred during periods when both rates and the dollar were trending lower simultaneously.

That relationship became one of the market’s most reliable intermarket signals: lower yields eased financial conditions and encouraged investors to buy stocks and other risky assets.

When the Relationship Starts to Feel Different

Recently, cracks have begun to appear in this otherwise dependable relationship between stocks and bonds.

During several of the market’s weakest sessions lately, the 10-Year Yield has fallen while equities also declined — meaning bonds rallied at the same time stocks struggled.

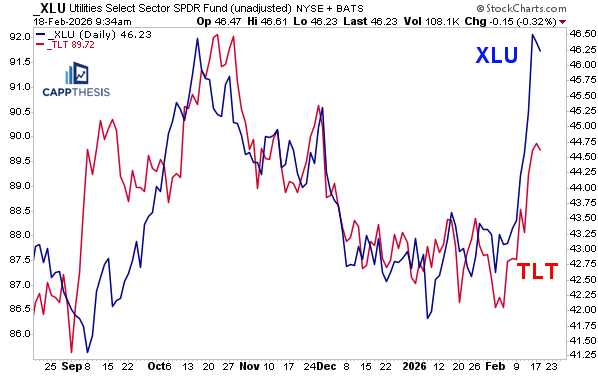

This dynamic stood out particularly last week, when defensive areas surged. Utilities (XLU) and long-duration Treasuries (TLT) advanced together, while leadership rotated toward traditionally defensive groups like Consumer Staples and Real Estate.

That combination is notable because it reflects something deeper than a simple rate-driven rally. Instead, it resembles a classic flight-to-safety environment, where investors prioritize capital preservation over growth exposure.

For much of the post-2022 period, falling yields represented optimism about inflation easing and policy becoming less restrictive. Now, falling yields may instead be signaling concern about growth, earnings durability, or broader market risk – should rates and stocks continue to fall together.

And that distinction matters.

A Historical Comparison: Early 2000

The current setup brings back memories of the early stages of the dot-com unwind — a period often remembered for speculative excess but less discussed for its inter-market behavior.

The backdrop of 2000 is well known. Companies with questionable fundamentals soared simply by attaching “.com” to their names, fueling one of history’s most dramatic speculative manias. When the bubble began to burst, technology stocks led the decline, but eventually the damage spread across the broader market. The bear market ultimately lasted until October 2003.

What receives far less attention is how interest rates behaved during that period.

Unlike 2022 — when yields surged higher amid inflation and aggressive Federal Reserve tightening — rates during the dot-com era were already peaking as equities topped out. The 10-Year Yield peaked in January 2000, roughly two months before both the NASDAQ and S&P 500 reached their highs in March.

From that point forward, something unusual happened: stocks and interest rates declined together for an extended period.

Rather than supporting equities, falling yields reflected deteriorating economic expectations and a migration toward safety. Bonds became the market’s preferred destination as risk assets unwound.

Correlations Don’t Break — They Mean-Revert

None of this is a prediction that today’s market will follow the same path. However, the comparison serves as an important reminder.

Market correlations are not permanent laws. They evolve, stretch, and sometimes reverse for extended periods — even years — before reverting to historical norms.

Thus, the assumption that falling yields must automatically support equities can become dangerous if the underlying reason for those falling yields changes.

If rates are declining because inflation pressures are easing, equities tend to benefit. But if rates fall because investors are seeking safety, the message is entirely different.

For now, the key question isn’t simply whether yields are falling — it’s why they are falling. And if leadership remains with defensive areas while growth sectors continue to struggle, the market may signal that this distinction is becoming increasingly important.

CappNotes offers a small window into the work we do at CappThesis - a technical analysis newsletter company focused on classical chart patterns, trend, and risk management. Explore the full range of CappThesis services here: