7/13/26

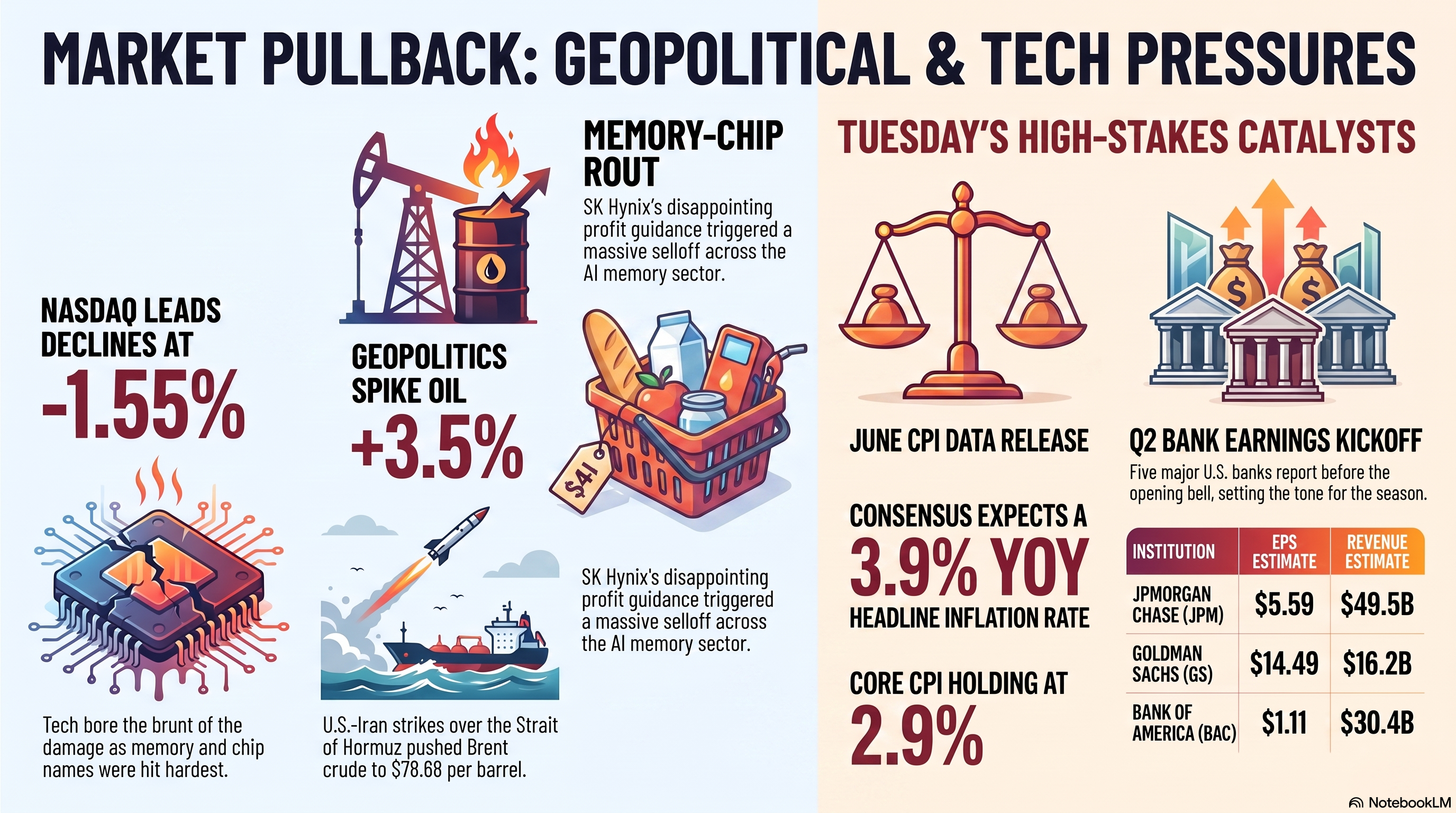

Stocks slid to start a pivotal week as renewed U.S.–Iran strikes over the Strait of Hormuz sent oil sharply higher, while a brutal memory-chip selloff sparked by SK Hynix’s (SKHY) disappointing profit guidance rattled the AI trade. Energy names were the one bright spot, cushioning the Dow as tech bore the brunt of the damage. All eyes now turn to Tuesday, when June CPI lands at the same moment as the season’s first wave of bank earnings.

What Happened Today

🔴 S&P 500 closed at 7,515.34, down 0.79%—pulling back from last week’s highs as risk-off spread across the tape.

🔴 Nasdaq Composite fell 1.55% (-408.43 points) to 25,873.18—the session’s biggest laggard as memory and chip names got hit hardest.

🔴 Dow Jones dropped 138.37 points (-0.26%) to 52,498.64—the smallest decline of the majors, cushioned by energy.

🔴 Russell 2000 lost 0.83% (-24.64) to 2,953.17—small-caps offered no shelter from the broader selling.

🟡 Breadth was mixed rather than uniformly negative—energy and a handful of defensive names advanced even as the indices closed lower.

Earnings

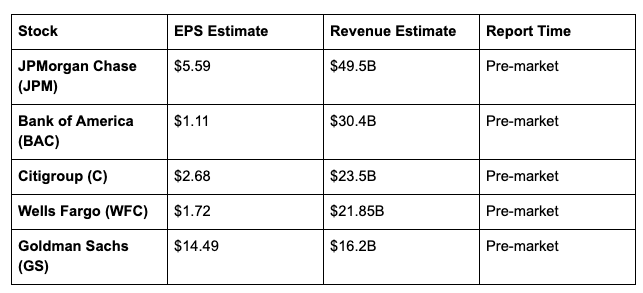

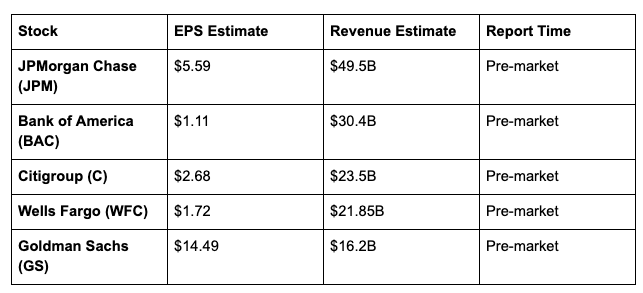

🟡 A quiet day on the earnings front—the real action starts tomorrow, when JPMorgan, Bank of America, Citigroup, Wells Fargo, and Goldman Sachs kick off Q2 bank earnings season before the open (full preview below in Tomorrow’s Calendar).

🟢 Delta Air Lines (DAL) and PepsiCo (PEP) both topped estimates last week, setting an encouraging tone heading into the bank-earnings deluge.

Macro/Policy

🔴 Fed rate-hike odds jumped as oil surged—Kalshi traders now price a 36% chance of a July hike, up from under 20% on Sunday, while CME’s FedWatch tool shows 46.5% odds of a 25bp hike on July 29.

🟡 Fed Governor Christopher Waller warned the central bank must not repeat the 2021–22 mistake of waiting too long to raise rates, though he cautioned against overcorrecting.

🟡 June CPI is due tomorrow at 8:30 AM ET—consensus looks for a soft headline (around -0.1% MoM, ~3.9% YoY) on falling June gasoline prices, but core CPI is expected to hold near 2.9% YoY, the number the Fed actually watches.

Geopolitics

🔴 The U.S. and Iran traded fresh strikes over the weekend and into Monday, with Iran declaring the Strait of Hormuz closed “until further notice”—a claim U.S. Central Command disputes.

🔴 President Trump announced the U.S. is reinstating a blockade on Iranian shipping through Hormuz and will seek a 20% toll on other cargo transiting the strait.

🔴 Iran retaliated against U.S. allies, including a reported strike on a Kuwaiti offshore drilling platform—the first direct hit on regional energy infrastructure in weeks.

🔴 Vessel traffic through Hormuz fell to a five-week low—just six ships transited Sunday versus a normal 18–22 daily crossings.

Foreign Markets

🔴 South Korea’s Kospi plunged roughly 9%, triggering a 20-minute circuit-breaker halt, as the memory-stock rout hit its epicenter.

🔴 SK Hynix shares fell more than 15% in Seoul—their steepest single-day drop on record—while Samsung Electronics dropped roughly 9–11%.

🔴 Brent crude jumped more than 3.5% to around $78.68/bbl on the renewed Hormuz tensions.

AI

🔴 SK Hynix (SKHY) U.S.-listed shares fell 8–9% in their second trading day after last week’s Nasdaq debut, after Korean brokerage KIS cut its Q2 profit forecast 8% below consensus on delayed HBM4 shipments.

🔴 The guidance miss cascaded through the AI memory trade: Micron (MU) fell roughly 5–6%, SanDisk (SNDK) tumbled 10–12%, Western Digital (WDC) dropped 7–8%, and the Roundhill Memory ETF (DRAM) sank 9%.

🔴 AppLovin (APP) slid 11.2% after analysts flagged a slow start to its e-commerce advertising expansion.

🟡 The selloff is being read as profit-taking and a “sell the news” reaction to SK Hynix’s oversubscribed U.S. offering rather than a break in the underlying AI-memory demand story, according to traders quoted in Bloomberg.

Corporate

🟢 Biogen (BIIB) rose 5.2% after a Truist upgrade citing optimism around its Alzheimer’s pipeline.

🟢 Agenus (AGEN) surged 95–108% after announcing an oversubscribed private placement of up to $340M to fund its colon-cancer immunotherapy trial.

🟢 Twin Vee PowerCats (VEEE) spiked well over 300% on a definitive merger agreement to privatize its marine business.

🟢 FuboTV (FUBO) gained about 11% after naming former Disney+ president Alisa Bowen as its new CEO.

Market Structure

🟡 No index-composition changes or trading-rule shifts of note today.

🟢 Leaders

Honeywell — top Nasdaq 100 gainer, up 7.5% on the day.

Intuit — led S&P 500 gainers, up 4.3%.

Biogen — up 5.2% on a Truist analyst upgrade.

Agenus — up over 95% on a private-placement financing.

LyondellBasell — added 4.1%.

🔴 Laggards

AppLovin — down 11.2% on e-commerce ad-growth concerns.

SK Hynix — fell roughly 9% in U.S. trading on a Q2 guidance cut.

SanDisk — dropped as much as 12.3% in the memory-sector selloff.

Western Digital — down 7–8% alongside memory peers.

Micron — fell 5–6% in sympathy with SK Hynix’s miss.

Commodities

🟢 WTI crude jumped 4.6% to $74.70/bbl, extending the Hormuz-driven rally as the U.S. and Iran continued exchanging strikes near the waterway.

🟢 Brent crude rose 4.5% to $79.46/bbl, closing in on its highest level since the conflict reignited.

🟡 Copper slipped 0.5% to $6.20/lb, essentially holding steady despite the broader risk-off tone.

🔴 Natural gas eased 1.8% to $2.89/MMBtu, pressured by mild weather forecasts and comfortable storage levels.

🔴 Silver dropped 2.3% to $58.42/oz, tracking gold lower on the same rate repricing.

🔴 Gold fell 2.6% to roughly $4,005/oz, giving back ground as rising Fed rate-hike odds outweighed the safe-haven bid.

Crypto

🔴 Bitcoin (BTC) slid to around $61,900, down roughly 3.3%, as risk-off flows hit crypto alongside equities.

🟡 A wave of leveraged long liquidations (~$73M) amplified the move; traders are watching whether Bitcoin holds the $61,000–$62,500 zone heading into tomorrow’s CPI print.

Prediction Markets

🔴 Kalshi’s odds of a July 29 Fed rate hike rose to 36%, up sharply from under 20% on Sunday, as oil prices jumped.

🟡 Polymarket’s ladder shows 81.5% odds of “no change” and 16.6% odds of a 25bp hike at the July meeting—still the base case, but shifting.

🟢 Polymarket prices a 74% chance of a permanent U.S.–Iran peace deal by year-end, suggesting traders still see the current escalation as contained rather than a full breakdown.

Volatility

🔴 VIX jumped roughly 14% to around 17.1, reflecting the Iran escalation and positioning ahead of tomorrow’s CPI/bank-earnings double header.

🟡 Still well below levels that would signal acute fear—front-end vol is bid into tomorrow’s event risk rather than broad-based panic.

Tomorrow’s Calendar

Tuesday, July 14 — June CPI + Q2 Bank Earnings

June CPI report — Bureau of Labor Statistics, 8:30 AM ET. Consensus: headline roughly -0.1% MoM / ~3.9% YoY; core CPI ~2.9% YoY.

Q2 bank earnings — all five below report before the market open:

BlackRock (BLK) and Morgan Stanley (MS) follow on Wednesday, July 15, also before the open.

No notable after-the-close reports Tuesday evening—Tuesday’s AMC slate is limited to small regional names (e.g., Equity Bancshares). Netflix (NFLX) doesn’t report until later in the week.

Positioning Read

Trend: S&P 500 at 7,515 is pulling back from last week’s highs; a clean CPI print and solid bank beats tomorrow could set up a retest of 7,575, while a hot print risks a slide toward 7,300–7,350.

Breadth: Weak today—memory and chip names dragged the tape lower, with energy as the only real offset.

Vol: VIX at 17.1 signals rising caution, not capitulation, heading into tomorrow’s twin catalysts.

Macro: Fed-hike odds are moving in real time with oil prices—any further Hormuz escalation feeds directly into the rate debate.

3 Scenarios

🟢 Bullish: June CPI cools as expected, the big banks beat on EPS and revenue with confident guidance, and Iran tensions show signs of de-escalating—stocks rebound toward 7,575 and vol eases back below 16.

🟡 Neutral: CPI lands in line, bank results are solid but unspectacular, and the Hormuz standoff continues without fresh escalation—indices grind sideways in a 7,450–7,550 range.

🔴 Bearish: Core CPI runs hot, at least one major bank disappoints on NIM or credit, and Iran escalates further—S&P 500 tests 7,300–7,350, VIX pushes toward 22–25, and memory/AI names extend losses.

Final Take

Monday was a preview of the stakes for Tuesday: a two-front risk-off session—Iran-driven oil spike on one side, a memory-chip guidance shock on the other—that left the S&P 500 down for a second session and pushed Fed rate-hike odds meaningfully higher for the first time in weeks.

None of today’s damage was catastrophic, and energy’s resilience shows the market isn’t in full flight-to-safety mode. But the setup into Tuesday is about as loaded as it gets:

June CPI and five bank earnings reports hit the tape within two hours of each other, with the Strait of Hormuz standoff still unresolved in the background. A soft CPI print paired with confident bank guidance could turn this into a one-day scare; a hot print or credit-quality wobble from any of the majors would confirm today’s selling as the start of something bigger.

Source: CNBC, Yahoo Finance, Reuters, Bloomberg, The Motley Fool, Trading Economics, Benzinga, IG, Kiplinger.

CappNotes offers a small window into the work we do at CappThesis - a technical analysis newsletter company focused on classical chart patterns, trend, and risk management. Explore the full range of CappThesis services here: