Summary

🟢 Wednesday was a “good news is good news” session — a second straight cooler-than-expected inflation print gave the market room to look past another round of US strikes on Iran.

Big Tech did the heavy lifting, with Apple (AAPL) hitting a fresh record high and the rest of the megacap cohort rallying on China AI approval and a broadening rotation out of semiconductors.

Financials had their own moment: Morgan Stanley (MS) and BlackRock (BLK) both blew past estimates, and PayPal (PYPL) exploded higher on a surprise $53 billion takeover bid from Stripe and Advent International.

Bonds and vol both rallied alongside stocks — yields eased and the VIX slid to its lowest levels of the summer — even as the Fed struck a still-cautious tone on inflation and the war in the Middle East showed no signs of cooling.

Major Indices & Breadth

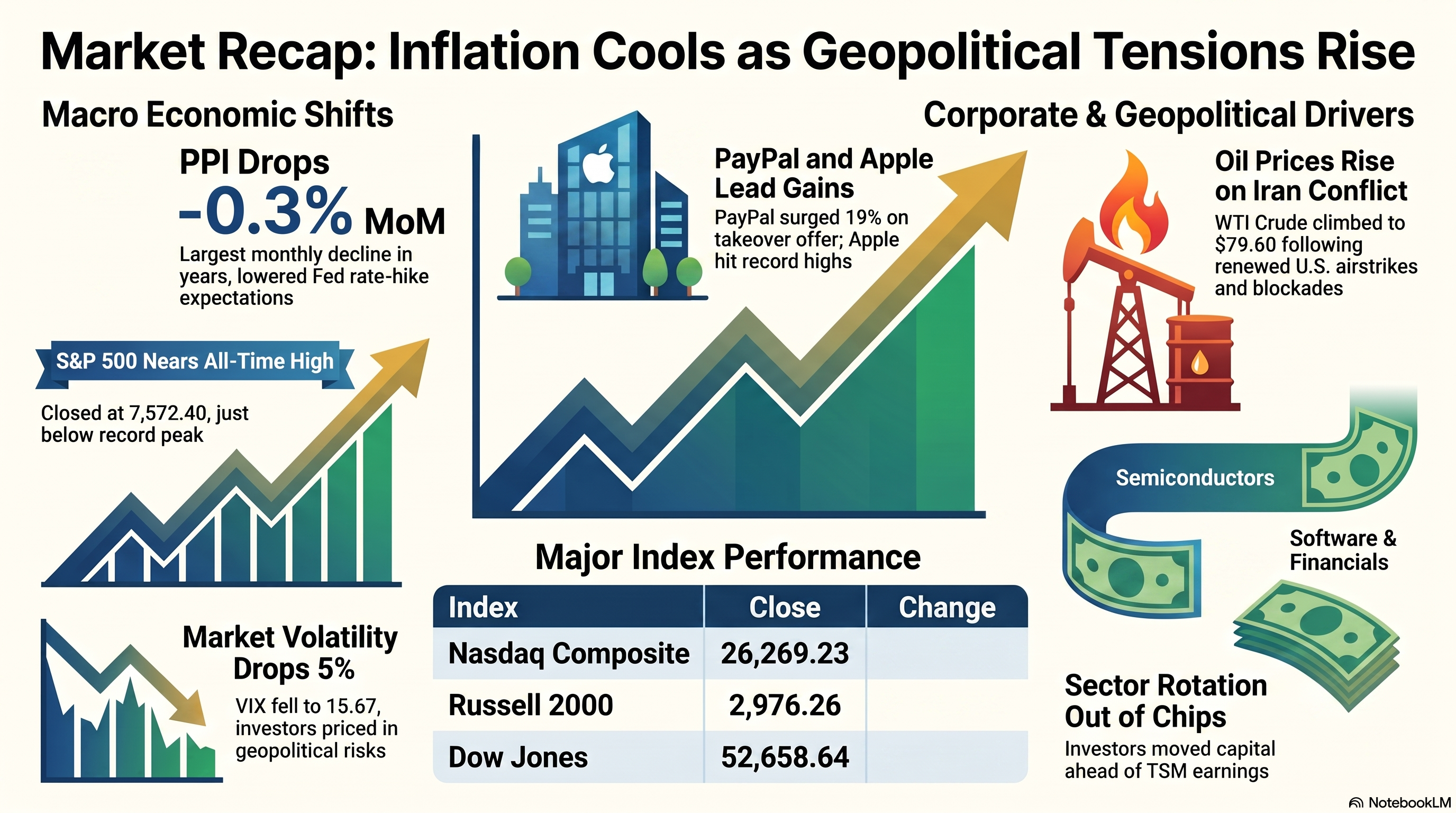

🟢 S&P 500 rose 0.38% to 7,572.40, a third positive session in the last four.

🟢 Nasdaq Composite gained 0.62% to 26,269.23, led by megacap tech.

🟢 Russell 2000 added 0.39% to 2,976.26, small-caps also catching a bid on the cooler inflation data.

🟢 Dow Jones Industrial Average rose 0.29% (+150.37 points) to 52,658.64.

🟡 Breadth was mixed under the surface — Big Tech and financials led, while semiconductors and memory names were a persistent drag all session.

🟢 Leaders

PYPL +17.20%

BLK +6.63%

AEHR +5.87%

AAPL +4.01%

GOOGL +3.60%

🔴 Laggards

SNDK -12.40%

MU -8.02%

WDC -7.70%

TRV -2.69%

CSCO -1.69%

Earnings

🟢 BLK posted adjusted EPS of $13.91 (beat $12.70 est.) on revenue of $7.08B (beat $6.77B est.), with AUM hitting a record $15.3T and operating margin of 45.9% — the highest in nearly five years. Shares jumped +6.63% (see Leaders).

🟢 MS reported record quarterly profit, with EPS of $3.46 (beat $2.94 est.) on revenue of $21.35B (beat $19.64B est.); profit rose 58% YoY on a 69% surge in equities trading revenue to a record $6.3B.

🟢 Johnson & Johnson (JNJ) beat estimates and shares rose on the print.

🟢 United Airlines (UAL) raised its full-year profit guidance to the high end of its prior range.

🟡 Additional notable earnings: ASML Holding (ASML), Bank of New York Mellon (BNY), Progressive (PGR).

AI

🟢 AAPL hit a fresh all-time high, +4.01%, after a report the company won approval to launch its generative AI features in China.

🟢 Alphabet (GOOGL), Microsoft (MSFT), Meta Platforms (META), and Amazon (AMZN) all rallied roughly 3% as investors rotated out of chips and into megacap AI platforms.

🔴 Micron (MU) fell 8.02% (see Laggards) as memory names gave back some of Tuesday’s rally; Lam Research (LRCX) and Advanced Micro Devices (AMD) each declined roughly 3%.

🔴 SpaceX (SPCX) fell below its IPO price for the first time, dropping under $135/share to a new all-time low — down roughly a third from its post-listing highs.

Corporate

🟢 PYPL surged 17.20% (see Leaders) after Stripe and private-equity firm Advent International made a joint $53 billion takeover bid, offering $60.50/share — a 28% premium to Tuesday’s close. PayPal’s board has not yet responded.

🔴 Yum! Brands (YUM) was on track for its worst week since December, down more than 5%, as a cyclospora outbreak linked to Taco Bell rattled investors.

Market Structure

🟡 Securitize gained roughly 15% after unveiling plans, in partnership with Cantor Fitzgerald & Co., to help public companies issue their stock on blockchain rails — a notable step toward tokenized equity infrastructure.

Macro/Policy

🟢 June PPI fell -0.3% MoM, the largest monthly decline in nearly a year, versus expectations for a flat reading; core PPI rose a softer-than-expected +0.2%.

🟡 The report followed Tuesday’s cooler CPI (+3.5% YoY, -0.4% MoM — the first monthly decline since 2020), reinforcing the case that inflation is decelerating.

🟡 Fed Chair Kevin Warsh reiterated the central bank has “no tolerance” for persistently elevated inflation, even as markets trimmed September rate-hike odds to roughly 50% from 60-70% pre-CPI (see Prediction Markets). The Fed’s Beige Book showed economic activity increasing at a slight-to-moderate pace.

Treasury Bonds

🟢 10-Year Treasury yield fell about 3bps to 4.555%, extending Tuesday’s post-CPI slide on the cooler PPI print (see Macro/Policy).

🟢 2-Year Treasury yield fell about 4bps to 4.145%, tracking reduced near-term Fed hike odds.

🟡 30-Year Treasury yield was little changed, down less than 1bp to 5.09%.

Geopolitics

🔴 The US launched a fresh, seven-hour wave of strikes on Iran — the fourth consecutive day of action — targeting military assets along Iran’s coastline near the Strait of Hormuz, while reinstating a naval blockade on Iranian ports.

🟡 President Trump abandoned a proposed 20% fee on cargo transiting Hormuz, saying lost revenue would be offset by future Gulf-state investment into the US; he also said Iran had signaled willingness to negotiate even as strikes continue.

🟡 House Republicans unveiled a $95 billion package covering Iran war funding, farm aid, and election-related spending.

Foreign Markets

🟡 Asia-Pacific markets were set for a mixed open Thursday: Nikkei 225 futures pointed lower (~67,890 vs. Wednesday’s 68,751.51 close), while Hang Seng futures were higher (~24,829 vs. 24,681.10 close).

🟢 Hong Kong’s Hang Seng rose 0.8% during the session, tracking broad Asian gains led by healthcare and real estate names.

🟡 European indices closed mixed Wednesday, with modest moves across the FTSE 100, DAX, and CAC 40.

Currencies

🔴 Dollar Index (DXY) fell 0.13% to 100.79, a second straight session of losses as the cooler PPI print weighed on the greenback (see Macro/Policy).

🟢 EUR/USD advanced toward 1.1408 as dollar weakness supported the euro.

🟢 GBP/USD climbed off session lows to around 1.3461 on the softer US inflation data.

🟢 USD/JPY eased to roughly 162.17 as the dollar broadly softened.

Commodities

🔴 WTI crude rose about 1.3% to $80.36, a one-month high, extending gains for a third session on Hormuz supply fears (see Geopolitics).

🔴 Brent crude climbed to roughly $85.44 on the same Iran-driven supply concerns.

🟡 Gold held near $4,066-4,077/oz, roughly flat on the day as dollar weakness offset easing safe-haven demand.

🟡 Silver traded sideways under pressure, testing support near $54.

Crypto

🟢 Bitcoin (BTC) rose toward $64,940, nearing $65,000 as softer inflation data improved risk sentiment.

🟢 Ethereum (ETH) gained 2.6% to $1,923.23.

🟢 Solana (SOL) added 0.3% to $77.35.

🟢 Spot Bitcoin and Ethereum ETFs saw combined inflows of more than $180 million.

Prediction Markets

🟡 Polymarket traders are pricing an 82% probability PayPal is acquired before 2027, and a 75% probability Stripe specifically closes a deal in 2026 (see Corporate).

🟡 Fed funds futures now price roughly a 50% probability of a September rate hike, down from 60-70% ahead of this week’s inflation data (see Macro/Policy).

Volatility

🟢 VIX fell 5.03% to 15.67, near its lowest levels of the summer, as cooling inflation data outweighed ongoing Iran headlines.

Tomorrow’s Calendar

UnitedHealth (UNH) reports before the bell.

State Street (STT) reports before the bell.

Netflix (NFLX) reports after the close.

Retail Sales (June), 8:30 AM ET.

Initial Jobless Claims, 8:30 AM ET.

Philadelphia Fed Manufacturing Index, 8:30 AM ET.

3 Scenarios

🟢 Bullish: Retail sales and jobless claims confirm the cooling-inflation narrative, broadening the rally beyond megacap tech; any sign of Iran de-escalation following Trump’s negotiation comments adds further tailwind — S&P 500 pushes toward 7,600+.

🟡 Neutral: Data comes in roughly in line, chip-versus-megacap rotation continues, and Iran strikes persist without meaningfully disrupting Hormuz shipping — indices grind sideways near current levels.

🔴 Bearish: A hot retail sales or jobless claims surprise revives September hike odds, while renewed Iran escalation disrupts Hormuz flows and sends oil sharply higher — S&P 500 retreats toward 7,450-7,500 as the semiconductor selloff broadens.

Final Take

Wednesday’s tape captured the tension defining this market right now: cooling inflation data is doing more to move stocks than an active war in the Middle East.

A second consecutive soft print — PPI following Tuesday’s CPI — gave traders enough cover to push September rate-hike odds down to a coin flip and rotate hard into megacap tech, even as the US carried out its fourth straight day of strikes on Iran.

Under the hood, financials had a standout day, with MS and BLK both posting records, while the PYPL takeover bid was a reminder that M&A appetite remains very much alive.

Thursday’s retail sales and jobless claims — plus earnings from UNH and NFLX — will be the next real test of whether this rotation has legs.

Source: CNBC, Reuters, Bloomberg, Yahoo Finance, NPR, CNN, ABC News, Fox News, U.S. Bureau of Labor Statistics, Trading Economics, TheStreet, CoinDesk, CryptoBriefing.

CappNotes offers a small window into the work we do at CappThesis - a technical analysis newsletter company focused on classical chart patterns, trend, and risk management. Explore the full range of CappThesis services here: