Summary

🔴 Stocks slipped for a second straight session as another round of strong chip earnings failed to calm nerves about the durability of AI infrastructure spending.

A batch of solid Dow-component results offered pockets of strength, with UnitedHealth (UNH) and GE Aerospace (GE) both topping estimates before the bell.

Treasury yields pushed higher and oil extended its climb as the US carried out a fifth consecutive night of strikes on Iran, keeping an energy risk premium embedded in the tape.

The day’s marquee event landed after the close, when Netflix’s (NFLX) second-quarter report — a narrow revenue miss paired with a soft near-term guide — sent shares sharply lower in after-hours trading and set a cautious tone heading into the heart of tech earnings season.

Major Indices & Breadth

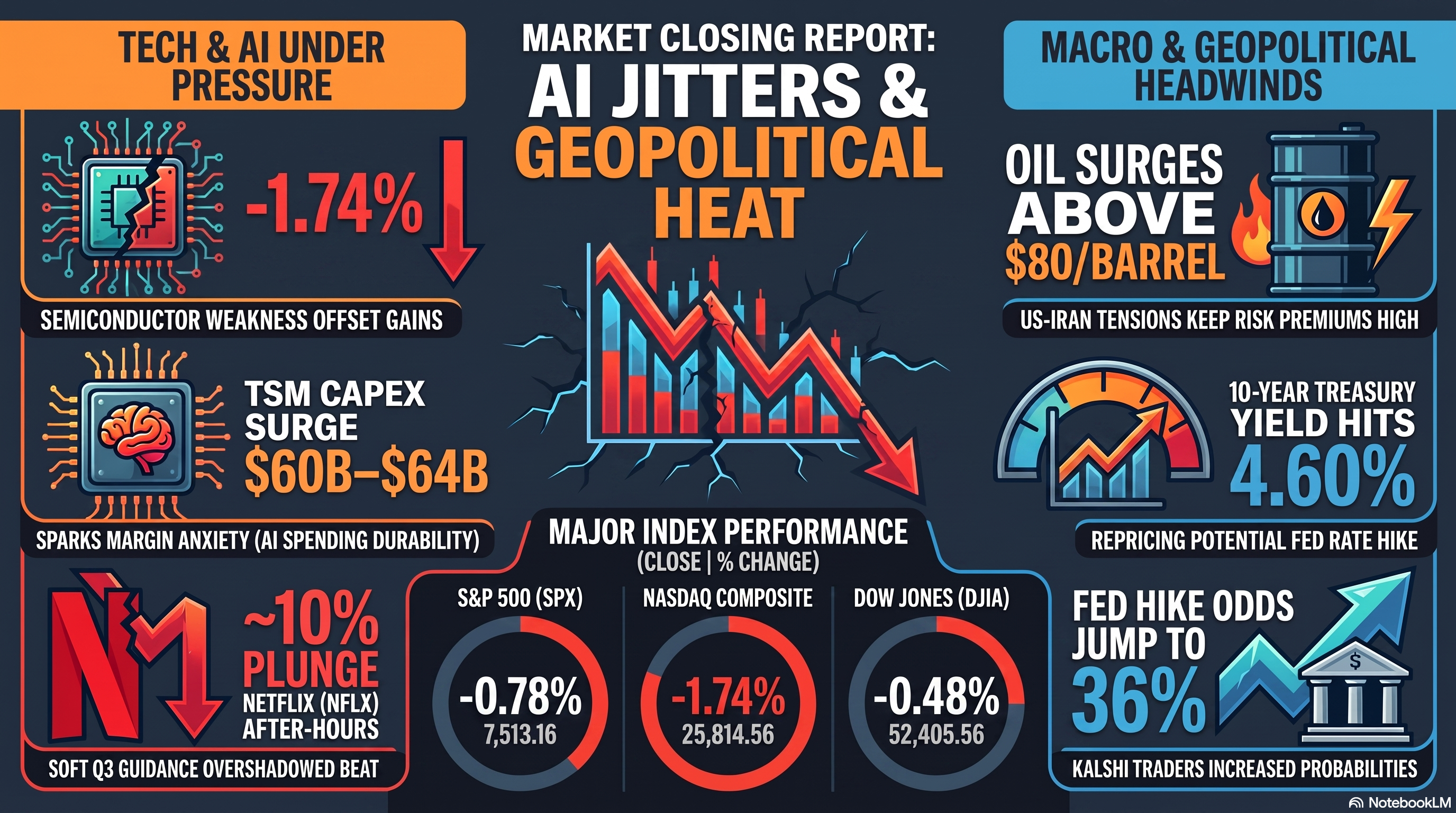

🔴 S&P 500 (SPX) closed at 7,513.16, -0.78% (-59.24 points) — as chip weakness offset gains in healthcare and defensives.

🔴 Nasdaq Composite fell -1.74% to 25,814.56 — the day’s worst performer as semiconductors extended their slide (see AI).

🔴 Dow Jones Industrial Average reversed earlier gains to close -0.48% (-253.08 points) lower at 52,405.56, dragged down late by GE’s post-earnings reversal.

🔴 Russell 2000 declined -0.30% to 2,967.22 — small-caps held up better than large-cap tech but still finished lower.

🟡 Breadth was mixed — a majority of individual S&P 500 names traded higher even as heavy chip-sector weighting pulled the cap-weighted indices down.

🟢 Leaders

ATAI +32.9%

MAN +13.0%

UNH +7.0%

JBHT +6.9%

CINF +6.8%

🔴 Laggards

WDC -8.8%

GLW -6.7%

MTG -5.7%

SNDK -5.4%

COHR -5.0%

NOW -4.7%

GE -4.4%

Earnings

🔴 Netflix (NFLX) reported Q2 revenue of $12.56B, a narrow miss versus the $12.587B estimate, while EPS of $0.80 beat the $0.79 consensus. Shares slid roughly -9.7% in after-hours trading as investors focused on a softer-than-expected Q3 guide rather than the headline beat. Management reaffirmed full-year 2026 revenue guidance of $50.7B-$51.7B and an operating margin near 31.5%, and the board expanded its buyback authorization by $25B.

🟡 Taiwan Semiconductor (TSM) posted record Q2 revenue and beat estimates, and raised full-year capex guidance to $60B-$64B from a prior $52B-$56B range. Shares still fell as investors weighed the heavier spending against margin pressure (see AI).

🟢 UnitedHealth (UNH) topped Q2 estimates and raised full-year profit guidance; shares +7.0%.

🔴 GE Aerospace (GE) posted adjusted EPS of $6.38 versus a $4.87 estimate on revenue of $112.03B, roughly flat year-over-year but above consensus. Shares fell anyway as investors rotated out of the beat.

🔴 United Airlines (UAL) beat on EPS with revenue in line, but issued soft third-quarter guidance on rising fuel costs; shares -3%.

🟢 Abbott Laboratories (ABT) beat EPS estimates and raised full-year guidance; shares +4%.

🟢 ManpowerGroup (MAN) beat estimates; shares +13.0%.

Additional notable earnings: Cincinnati Financial (CINF), J.B. Hunt Transport Services (JBHT), Corning (GLW) [missed], Sandisk (SNDK) [soft guide], ServiceNow (NOW) [soft], MGIC Investment (MTG) [missed], Coherent (COHR) [missed].

AI

🔴 Chip stocks fell broadly for a second straight session as TSM’s stronger-than-expected results and raised capex guidance (see Earnings) failed to reassure investors already anxious about the durability of AI infrastructure spending.

🔴 Micron Technology (MU) fell -5.2%; Western Digital (WDC) and Sandisk (SNDK) (see Laggards) led memory and storage names lower.

🔴 Advanced Micro Devices (AMD) and Intel (INTC) also declined amid the broader semiconductor selloff.

🟡 South Korea’s move to prohibit leveraged ETFs tied to speculative tech names, plus signals from ASML about more efficient chipmaking tools, added to concerns that AI capex growth could plateau.

🔴 SpaceX (SPCX) shares remain below their IPO price for a second session as investors weigh Chinese launch competition and a looming increase in tradeable share supply by early August.

Corporate

🟢 Uber (UBER) agreed to acquire Delivery Hero for $14.8B; shares +3%.

🟡 Eli Lilly (LLY) agreed to acquire AtaiBeckley (ATAI) for $3.8B; ATAI surged (see Leaders) while LLY slipped -1% on deal and dilution concerns.

Market Structure

🟡 No major index rebalancing, listing-rule, or trading-hour changes reported today.

Macro/Policy

🟡 June retail sales rose 0.2% month-over-month, below the 0.3% consensus, weighed down by lower gasoline spending, though core components were firmer.

🟢 Weekly initial jobless claims fell to 208,000 for the week ended July 11, below the 218,000 estimate and an over-two-month low — a sign the labor market remains resilient.

🔴 The combination of a still-tight labor market and rising energy costs from the Iran conflict (see Geopolitics) keeps the Fed on a hawkish footing; markets are pricing meaningfully higher odds of a July rate hike (see Prediction Markets).

Treasury Bonds

🔴 10-Year Treasury yield rose to roughly 4.60%, approaching the near-two-month high of 4.62% set July 13, as markets positioned for a possible Fed hike.

🔴 2-Year Treasury yield also pushed higher, tracking to around 4.25% as short-end rates reprice for hike risk.

🟡 30-Year Treasury yield firmed to roughly 5.10%, keeping the curve broadly stable even as the front end repriced.

🔴 The move higher across the curve tracks the same resilient-data-plus-energy-shock story driving Fed hike odds (see Macro/Policy).

Geopolitics

🔴 US forces conducted a fifth consecutive night of strikes on Iran, continuing an effort to degrade Tehran’s military capabilities and secure shipping through the Strait of Hormuz.

🟡 The Wall Street Journal reported Trump was briefed by aides on options to expand the conflict, including intensified bombing and the possible deployment of ground forces.

🔴 The renewed escalation has reversed much of the relief rally that followed the earlier interim ceasefire, keeping energy prices elevated (see Commodities) and reinforcing hawkish Fed expectations (see Macro/Policy).

Foreign Markets

🟡 European markets edged lower following another volatile overnight session in Asia’s tech-heavy indexes, tracking the same chip-sector unease weighing on Wall Street.

🟡 India’s Sensex finished essentially flat at 77,186.87, while the Nifty slipped -0.02% to 24,072.75, as investors weighed geopolitical uncertainty against swings in crude prices.

🟡 Broader Asian trading was cautious, with tech-heavy benchmarks pressured by the same semiconductor valuation concerns hitting US markets (see AI).

Currencies

🟢 US Dollar Index (DXY) firmed to roughly 100.7 as investors favored the dollar amid rising Treasury yields and hawkish Fed repricing.

🔴 EUR/USD held near $1.14, easing modestly as the dollar firmed.

🟢 USD/JPY traded near ¥162, with the yen still struggling to mount a sustained recovery against elevated dollar strength.

🔴 GBP/USD softened toward the $1.35 area alongside the broader dollar advance.

Commodities

🔴 WTI crude traded above $80/barrel, extending a more than 11% gain over the prior three sessions as the US-Iran conflict escalated (see Geopolitics).

🔴 Brent crude closed just below $85/barrel, tracking the same Strait of Hormuz risk premium.

🔴 Gold fell toward $4,000/ounce, its lowest level since November 2025, as rising yields and a firmer dollar pressured the non-yielding metal even amid geopolitical risk.

🔴 Silver also declined, tracking gold’s pullback (see above) as the dollar and yields moved higher.

Crypto

🟢 Bitcoin (BTC) traded around $64,600, holding most of this week’s gains after a softer-than-expected US inflation print sparked a reversal in institutional ETF flows.

🟢 Ethereum (ETH) traded near $1,900, with some strategists flagging it as “increasingly compelling” as it leads bitcoin in the week’s recovery.

🟡 Spot Bitcoin ETFs saw modest net inflows today, reversing a prior ten-day, $2.73B outflow streak, though the Crypto Fear & Greed Index remains in “Fear” territory.

Prediction Markets

🔴 Kalshi traders put the odds of a Fed rate hike at the July 29 meeting at roughly 36%, up sharply from under 10% earlier this month, as the renewed Iran escalation lifted oil and inflation expectations.

🟡 CME’s FedWatch tool shows a similar 46.5% probability of a quarter-point hike this month, reflecting the same repricing (see Macro/Policy).

🟡 Separate 2026 full-year hike contracts on Kalshi and Polymarket remain in the 53-54% range, little changed on the day.

Volatility

🔴 VIX rose 8.48% to 17.00, reflecting elevated but not extreme risk awareness as chip weakness, rising yields, and the Iran escalation weighed on sentiment simultaneously.

🟡 Options markets had priced an outsized post-earnings swing for NFLX; the roughly -9.7% after-hours move (see Earnings) came in within that expected range.

🟡 Term structure remains elevated into a busy stretch of tech earnings, with implied volatility likely to stay bid through next week’s reports.

Tomorrow’s Calendar

American Express (AXP) and Schlumberger (SLB) report earnings before the bell Friday.

No major economic data releases are scheduled for Friday.

Geopolitical watch: any further escalation or de-escalation signal from the Iran conflict could move oil and yields sharply in either direction over the weekend.

Markets will continue digesting the wave of tech earnings, including reaction to Netflix’s (NFLX) guidance miss, as the sector searches for its next catalyst.

3 Scenarios

🟢 Bullish: The NFLX guidance miss is read as company-specific rather than sector-wide; oil pulls back on any Iran de-escalation signal; chip names stabilize as investors look past TSM’s capex raise toward the underlying demand backdrop — indices reclaim Thursday’s losses into next week.

🟡 Neutral: Chip-sector jitters persist into next week’s earnings slate; oil and yields stay elevated on an unresolved Iran conflict; the market grinds sideways as strong non-tech earnings offset AI-trade caution.

🔴 Bearish: The Iran conflict escalates further, pushing oil and yields sharply higher; NFLX’s miss is read as an early warning for consumer-facing tech spending; chip weakness spreads into the broader Nasdaq, pressuring the S&P 500 toward its recent lows.

Final Take

Thursday’s session captured the tension currently defining this market: strong individual earnings results running into a market unwilling to reward them while chip valuations and geopolitical risk stay elevated.

UnitedHealth (UNH) and TSM both delivered clean beats, yet neither could anchor sentiment against the drag from Treasury yields near two-month highs and oil pushing back above $80 on a fifth night of US strikes on Iran.

Netflix’s (NFLX) after-hours slide adds a fresh data point heading into a packed stretch of tech earnings — a reminder that guidance, not the headline print, is what this market is trading on right now.

With the Fed’s July 29 decision still a coin flip by some measures (see Prediction Markets), the next several sessions of data and earnings carry outsized weight for where risk appetite heads into August.

Source: CNBC, Yahoo Finance, Bloomberg, TheStreet, Trading Economics, Reuters.

CappNotes offers a small window into the work we do at CappThesis - a technical analysis newsletter company focused on classical chart patterns, trend, and risk management. Explore the full range of CappThesis services here: