Closing Look - 7/17/26

Stocks closed out a rough week Friday as a deepening semiconductor rout...

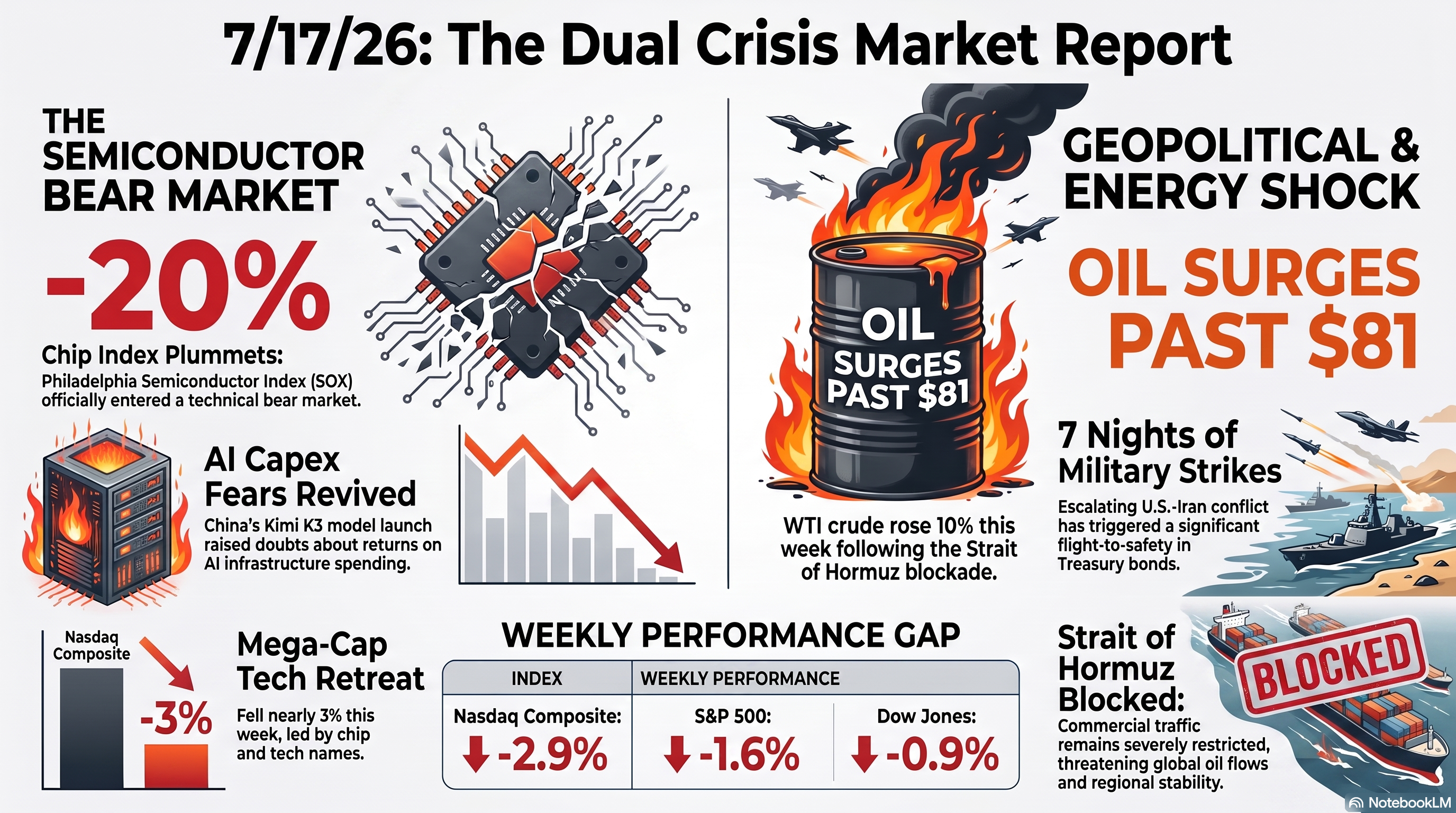

Summary

🔴 Stocks closed out a rough week Friday as a deepening semiconductor rout collided with a seventh straight night of US–Iran strikes.

The Philadelphia Semiconductor Index tipped into a technical bear market, down more than 20% from its June record, after Chinese startup Moonshot unveiled its Kimi K3 model and revived fears that AI infrastructure spending has outrun near-term returns.

Netflix (NFLX) extended Thursday’s post-earnings slide after a soft Q3 revenue outlook, while memory and storage names bore the brunt of the chip selloff.

Energy was the lone pocket of strength as oil jumped on renewed Strait of Hormuz tensions, and Treasury yields eased on the flight to safety.

All three major averages finished the week lower, with the Nasdaq’s nearly 3% weekly decline pacing the retreat.

Major Indices & Breadth

🔴 Russell 2000 (RUT) closed at 2,962.99, -0.39%—small-caps held up best, insulated from the mega-cap chip unwind.

🔴 Dow Jones (DJI) fell 406.55 points (-0.77%) to 52,146.42, down about 0.9% on the week.

🔴 S&P 500 (SPX) dropped -1.01% to 7,457.69, off roughly 1.6% for the week.

🔴 Nasdaq Composite (IXIC) led the downside, sliding -1.40% to 25,520.24—down nearly 2.9% on the week as chip and mega-cap tech names took the worst of it.

🟢 Leaders

TRV +6.4%

UNH +2.6%

WMT +2.1%

ABT +1.9%

🔴 Laggards

SKHY -13.0%

SNDK -12.6%

ISRG -12.4%

STX -10.0%

SNPS -9.8%

NFLX -7.6%

Earnings

🔴 Netflix (NFLX) posted a Q2 in-line beat—EPS $0.80 vs. $0.79 est., revenue $12.56B vs. $12.58B–$12.59B est.—but Q3 revenue guidance of $12.86B (+11.7%) undershot the ~$13B Street estimate, and shares extended Thursday’s after-hours slide into a double-digit weekly decline.

🟢 UnitedHealth Group (UNH) blew past estimates with Q2 EPS of $6.38 vs. $4.94 expected, the standout beat of the day.

🟢 Abbott Laboratories (ABT) beat on EPS ($1.31 vs. ~$1.28–1.29 est.) despite a slight revenue miss, and raised full-year adjusted EPS guidance to $5.45–$5.60.

🔴 Intuitive Surgical (ISRG) beat on both lines—revenue +19% to $2.89B, adjusted EPS +28% to $2.80—but held rather than raised procedure-growth guidance at 13.5%–15.5%, and flagged slowing U.S. procedure volume; shares still sank double digits.

🟡 Additional notable earnings: Synopsys (SNPS), SanDisk (SNDK), Seagate Technology (STX), Western Digital (WDC), Micron Technology (MU)—memory and storage names broadly weak on read-through from the chip selloff rather than company-specific misses (see AI).

AI

🔴 The Philadelphia Semiconductor Index (SOX) fell as much as 5.7% intraday, pushing its drawdown from the late-June record above 20%—the technical threshold for a bear market—and capping an 11% weekly decline, the worst chip rout since the April 2025 tariff selloff.

🔴 Chinese AI startup Moonshot released its Kimi K3 model, a 2.8-trillion-parameter open-weight system competitive with leading U.S. models, reviving “DeepSeek moment” fears about the payoff on hyperscaler AI capex.

🔴 SK Hynix ADR (SKHY) -13.0%, SanDisk (SNDK) -12.6%, Seagate Technology (STX) -10.0%, Western Digital (WDC) -9.0%, and Micron (MU) -5% to -6.7% led memory/storage names lower.

🔴 Synopsys (SNPS) fell -9.8% and Intel (INTC) and AMD each dropped roughly 4%–5% as the selloff broadened beyond memory into design software and logic chips.

🟡 Nvidia (NVDA) was more resilient relative to peers, down roughly 2–4% intraday, while Broadcom (AVGO) has shown relative outperformance this week.

🟡 Traders are watching whether next week’s hyperscaler and chip earnings (see Tomorrow’s Calendar) reaffirm 2026 AI capex plans or add to the unwind.

Corporate

🟡 Uber (UBER) shares dipped in premarket trading after announcing it will acquire Delivery Hero in a deal valuing the German company at $14.8B, a move that would create the largest food-delivery group outside China.

🔴 Coca-Cola (KO) slipped after a reported ransomware attack on its Fairlife milk subsidiary.

🔴 SpaceX (SPCX) shares fell further, a day after an aborted Starship test-flight attempt in Texas, extending choppy post-IPO trading.

Market Structure

🟡 No major S&P 500, Dow, or Nasdaq-100 index-composition changes or trading-rule updates today; the next scheduled quarterly index rebalance falls in September.

Macro/Policy

🟡 June retail sales came in roughly in line with expectations, with lower gasoline prices weighing on receipts even as auto and online retail spending stayed firm.

🟢 Weekly initial jobless claims fell to a two-month low of 208K.

🟢 Preliminary July University of Michigan consumer sentiment topped expectations, a bright spot for the domestic growth narrative.

🟡 Markets have largely priced out a July 29 Fed rate hike after softer June CPI and PPI prints, though expectations remain split on a possible September move (see Prediction Markets).

🟡 Fed Chair Kevin Warsh reiterated that price levels remain “too high” and that inflation risk has eased modestly since he took the helm in June, without signaling a near-term policy shift.

Treasury Bonds

🟢 10-Year Treasury yield fell 3 bps to 4.537% as investors rotated into safety amid the equity selloff.

🟢 30-Year Treasury yield eased more than 3 bps to 5.061%, tracking the broader flight-to-quality bid tied to the Iran escalation.

Geopolitics

🔴 U.S. Central Command carried out a seventh consecutive night of strikes against Iran, targeting military and logistics infrastructure as part of an effort to “continue degrading Iranian military capabilities.”

🔴 Iran struck a water desalination plant in Kuwait, exposing regional water-supply vulnerability, while U.S. forces also hit additional bridge infrastructure inside Iran.

🔴 Commercial traffic through the Strait of Hormuz remains severely restricted amid the reinstated U.S. naval blockade of Iranian ports, keeping the key oil chokepoint effectively closed to normal flows.

🟡 Qatar and Bahrain both activated air-defense sirens this week amid intercepted Iranian strikes, underscoring the risk of the conflict spreading to U.S. Gulf allies.

Foreign Markets

🔴 Taiwan’s stock market (TWSE) dropped roughly 6.5% as TSMC (TSM) and other chipmakers were dragged into the global semiconductor selloff.

🔴 Japan’s Nikkei 225 fell about 4% as heavy selling hit chipmakers and AI-related names; SoftBank -9.2%, Tokyo Electron -9.0%, and Advantest -9.4% led declines, while Kioxia plunged over 14% after a Texas jury ordered it to pay $229M in a patent case.

🟡 South Korean markets were closed for a public holiday.

Currencies

🟡 The Dollar Index (DXY) held roughly flat near 100.7, still on track for a weekly decline as softer U.S. inflation data trimmed near-term Fed rate-hike expectations, even as Iran-driven safe-haven flows offered some support.

🟡 The euro and British pound both gained modestly on the week against the dollar as Fed hike odds receded (see Prediction Markets).

Commodities

🔴 WTI crude (CL) jumped roughly 3–4% to above $81/barrel, up more than 10% on the week, as the reinstated Hormuz blockade and continued U.S.-Iran strikes threatened regional oil flows (see Geopolitics).

🟢 Gold rose about 0.5%–0.9% to roughly $4,005–$4,020/oz on safe-haven demand tied to the equity selloff and Middle East escalation.

🔴 Silver slipped about 0.6% to roughly $55.81/oz, a rare pullback after a strong recent run.

Crypto

🔴 Bitcoin (BTC) slipped to roughly $63,700–$64,000, down modestly on the day as risk-off flows in equities spilled into digital assets.

Prediction Markets

🟡 Polymarket’s “Fed Decision in July” ladder shows an 81.5% probability of no rate change at the July 29 meeting versus 16.6% for a 25bp hike, though those odds have been volatile amid the ongoing Iran escalation (see Macro/Policy).

🔴 Kalshi traders have pushed July hike odds up to roughly 36%, from under 20% a week earlier, as oil-driven inflation risk builds.

🟢 Polymarket separately prices roughly a 74% chance of a durable U.S.-Iran peace deal by year-end, suggesting traders still view the current escalation as contained rather than an open-ended war.

Volatility

🟡 VIX rose to roughly 18.0, up about 8% on the day and nearly 20% on the week, still below the 20-level “fear threshold” but reflecting fast-eroding complacency.

🔴 The chip-driven SOX bear market (see AI) is the dominant driver of this week’s vol repricing, with front-end options positioning bid into next week’s hyperscaler and Intel (INTC) earnings.

Tomorrow’s Calendar

Monday, July 20: Quiet session—no major scheduled earnings or economic releases; markets continue to digest weekend developments in the Iran conflict.

Tuesday, July 21: Alphabet (GOOGL) and Tesla (TSLA) report after the close; also reporting: AT&T (T), CSX Corp (CSX), Kinder Morgan (KMI), Philip Morris International (PM), Texas Instruments (TXN).

Wednesday, July 22: Honeywell (HON), Lockheed Martin (LMT), RTX Corp (RTX), T-Mobile US (TMUS), Union Pacific (UNP), American Airlines (AAL), Blackstone (BX) report.

Thursday, July 23: Intel (INTC) reports after the close; also reporting: Verizon (VZ), Exxon Mobil (XOM), American Express (AXP), NextEra Energy (NEE).

Wednesday, July 29: FOMC rate decision, 2:00 PM ET, followed by Chair Warsh’s press conference.

3 Scenarios

🟢 Bullish: Iran signals de-escalation over the weekend, oil gives back this week’s spike, and next week’s hyperscaler earnings reaffirm AI capex plans—chip names stabilize and the SOX finds a floor near current levels.

🟡 Neutral: The Hormuz standoff continues without further escalation, oil holds in the low-$80s, and markets grind sideways into next week’s Alphabet/Tesla and Intel reports as investors await clearer AI-capex signals.

🔴 Bearish: Iran strikes a U.S. Gulf ally directly or further disrupts Hormuz shipping, oil breaks above $85, and the chip bear market deepens as hyperscaler earnings disappoint on AI spending—VIX pushes back toward the low-20s.

Final Take

Friday closed out a week defined by two converging pressures: a chip sector that ran too far, too fast, and a war that keeps refusing to de-escalate.

The SOX’s slide into a bear market is the more structural story—Kimi K3 gave traders a reason to question AI-capex payback timelines, but the unwind was already building after a 105% run off the March low.

Oil’s surge past $81 and the seventh straight night of U.S.-Iran strikes are the more acute risk, and Treasury yields easing on safety flows shows the market is treating this as a real macro threat rather than background noise.

Netflix’s guidance miss added a company-specific wrinkle, but it’s the broader rotation out of the most crowded AI trades that defined the week.

Bottom line: next week’s Alphabet, Tesla, and Intel reports—plus whatever happens over the weekend in the Gulf—will determine whether this was a healthy reset or the start of something more durable.

Source: CNBC, Bloomberg, TheStreet, Yahoo Finance, The Motley Fool, Trading Economics, Reuters, CBS News, Investing.com, Polymarket, Kalshi.

CappNotes offers a small window into the work we do at CappThesis - a technical analysis newsletter company focused on classical chart patterns, trend, and risk management. Explore the full range of CappThesis services here: