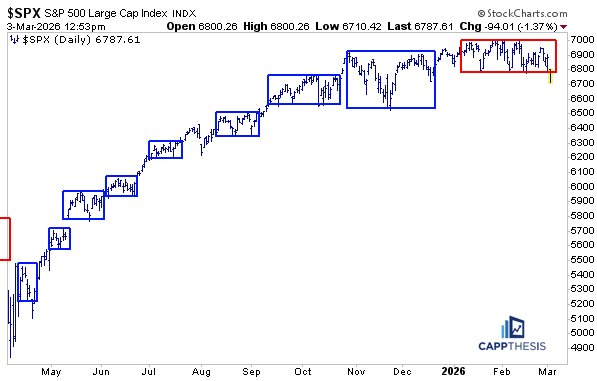

Given this week’s early price action, the S&P 500 now is testing the lower boundary of its latest trading range — what we classify as a trading box.

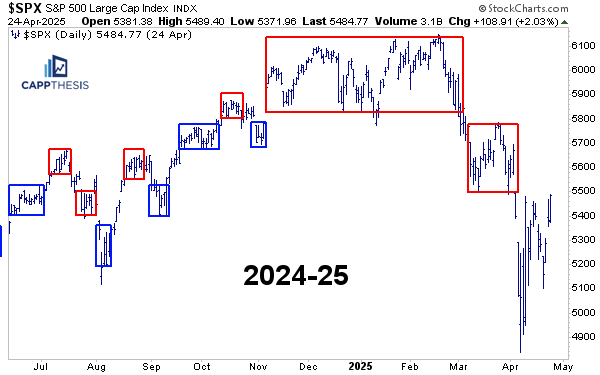

As most readers know, we view these ranges as important reference points for risk and opportunity. The last time we saw a clear trading box break down was during the February–April 2025 period. That makes this development noteworthy.

We’ll be writing about it much more in the coming days and weeks as things evolve.

Given how often we discuss trading boxes, I recently went back and re-read the book where the concept originated — How I Made $2,000,000 in the Stock Market by Nicolas Darvas. The appeal of Darvas’ work is that the framework is remarkably simple yet highly disciplined. His premise was straightforward: buy strength when price breaks out of a clearly defined trading range — the “box.”

As Darvas famously said:

“I buy high and sell higher.”

That sounds obvious, but psychologically it’s difficult to execute. Many investors hesitate to buy higher prices, especially after watching a stock previously fail near resistance. Buying a breakout often feels uncomfortable because it requires acting when price already appears extended. Darvas understood that discomfort was actually part of the edge.

He focused on stocks capable of meaningful movement — names with volatility and upside potential. His insight was that highly erratic stocks don’t necessarily attract attention because volatility is expected. Nothing about their behavior stands out. But when a stock becomes quiet and confined within a range, it fades from attention. That period of neglect is often what sets up the next meaningful move.

Darvas therefore searched for stocks already in established uptrends that had paused and formed orderly consolidations. If a stock continued trading between 50 and 60, for example, he ignored it. But the moment it pushed above 60 — escaping the box — it became actionable. Importantly, he prepared in advance. Once the box was defined, he placed two orders: a buy stop above the range and a protective stop just below it. The decision-making was done beforehand; execution became mechanical.

As he later explained:

“The main reason I made money was because I disciplined myself to follow a system.”

Sound familiar? This is essentially what the SPX has been doing for more than two months. The index has oscillated inside a clearly defined range, frustrating both bulls and bears while building energy beneath the surface. Because price must eventually forcefully resolve above or below the box, the day-to-day volatility inside the range should never overly concern us. What mattered (and continues to matter) is being prepared to adjust positioning once a confirmed break occurs.

Darvas captured this mindset perfectly:

“I never argue with the tape.”

And while the index has been stagnant until now, the underlying market tells a far more complex story. With 503 individual stocks driving movement, internal dispersion has been significant. Some areas continue pressing to new highs, while others have experienced deep drawdowns. Numerous studies on financial social media channels recently have highlighted just how historically bifurcated participation has become — a reminder that index stability can mask substantial rotation underneath.

Despite all these crosscurrents, the key takeaway is that none of the recent twists and turns had materially changed the SPX’s technical condition. For over two months, price structure remained intact. Momentum shifts have been short-lived, breadth swings have reversed quickly, and every attempted move has reverted back into the range up to this point. Eventually, however, consolidation gives way to expansion. The box is defined — now we wait for resolution.

Another important aspect of Darvas’ approach was his strict adherence to process. He only bought stocks; he did not short. He also avoided selling based on price targets, instead relying exclusively on stop losses to manage risk and protect capital.

As he observed:

“Losses never bothered me after I learned to cut them quickly.”

While he paid little attention to macro commentary or broad indices, he recognized when conditions changed — specifically when his breakout trades began failing more frequently. At the time, this was frustrating. He followed his rules, took small losses, and continued executing his system. Only later did he realize those repeated stop-outs coincided with what he described as a baby bear market from 1957-1958. Stocks he purchased near 60 and exited near 55 eventually collapsed toward 30 — a dynamic not unlike what we’ve recently seen in certain software and crypto-related names after failed momentum phases.

Darvas didn’t turn bearish based on opinion. He simply stepped aside because the market stopped producing the types of constructive patterns his strategy required — reinforcing another of his core beliefs:

“The market is never wrong — opinions often are.”

Markets evolve every year and look dramatically different across decades. Technology changes, participants change, and narratives change. But the core principles remain constant: define risk, follow your process, and let price — not emotion — dictate your actions.

Or, as Darvas summarized best:

“I made my money by sitting, not thinking.”